All Categories

Featured

Table of Contents

Section 691(c)( 1) offers that an individual who includes an amount of IRD in gross earnings under 691(a) is enabled as a reduction, for the exact same taxed year, a part of the estate tax paid by factor of the inclusion of that IRD in the decedent's gross estate. Generally, the quantity of the deduction is computed making use of inheritance tax values, and is the amount that bears the exact same proportion to the estate tax obligation attributable to the net worth of all IRD items included in the decedent's gross estate as the worth of the IRD included because individual's gross earnings for that taxable year births to the value of all IRD items included in the decedent's gross estate.

Rev. Rul., 1979-2 C.B. 292, resolves a situation in which the owner-annuitant acquisitions a deferred variable annuity contract that supplies that if the proprietor passes away prior to the annuity starting date, the named beneficiary might choose to get the present gathered value of the contract either in the form of an annuity or a lump-sum repayment.

Rul. 79-335 wraps up that, for functions of 1014, the agreement is an annuity explained in 72 (as then basically), and for that reason obtains no basis modification because the proprietor's death since it is regulated by the annuity exception of 1014(b)( 9 )(A). If the recipient chooses a lump-sum payment, the extra of the amount obtained over the amount of factor to consider paid by the decedent is includable in the beneficiary's gross income.

Rul. Had the owner-annuitant gave up the contract and obtained the amounts in unwanted of the owner-annuitant's financial investment in the agreement, those amounts would certainly have been income to the owner-annuitant under 72(e).

Is there tax on inherited Annuity Interest Rates

Similarly, in today situation, had A gave up the agreement and obtained the amounts moot, those amounts would certainly have been earnings to A under 72(e) to the extent they exceeded A's financial investment in the contract. Accordingly, amounts that B gets that surpass A's financial investment in the contract are IRD under 691(a).

, those quantities are includible in B's gross earnings and B does not get a basis change in the agreement. B will certainly be qualified to a reduction under 691(c) if estate tax obligation was due by reason of A's death.

The holding of Rev. Rul. 70-143 (which was revoked by Rev. Rul. 79-335) will certainly remain to make an application for delayed annuity contracts purchased prior to October 21, 1979, consisting of any payments put on those agreements according to a binding commitment became part of before that date - Lifetime annuities. PREPARING info The major author of this earnings ruling is Bradford R

Q. Just how are annuities taxed as an inheritance? Is there a difference if I acquire it straight or if it mosts likely to a trust fund for which I'm the recipient?-- Preparation aheadA. This is a great inquiry, however it's the kind you should require to an estate planning lawyer who knows the details of your circumstance.

For instance, what is the partnership in between the departed proprietor of the annuity and you, the recipient? What sort of annuity is this? Are you making inquiries about revenue, estate or estate tax? We have your curveball inquiry regarding whether the result is any different if the inheritance is with a trust fund or outright.

We'll think the annuity is a non-qualified annuity, which suggests it's not component of an IRA or various other professional retired life plan. Botwinick said this annuity would certainly be included to the taxable estate for New Jersey and federal estate tax purposes at its day of death worth.

Taxes on Annuity Rates inheritance

resident spouse surpasses $2 million. This is called the exemption.Any quantity passing to an U.S. citizen partner will be completely exempt from New Jersey inheritance tax, and if the proprietor of the annuity lives throughout of 2017, after that there will be no New Jacket inheritance tax on any kind of quantity since the estate tax obligation is set up for abolition beginning on Jan. After that there are government estate taxes.

The present exemption is $5.49 million, and Botwinick said this tax is possibly not going away in 2018 unless there is some significant tax obligation reform in a genuine hurry. Fresh Jacket, federal inheritance tax law provides a full exception to amounts passing to enduring united state Following, New Jersey's inheritance tax.Though the New Jersey estate tax is scheduled

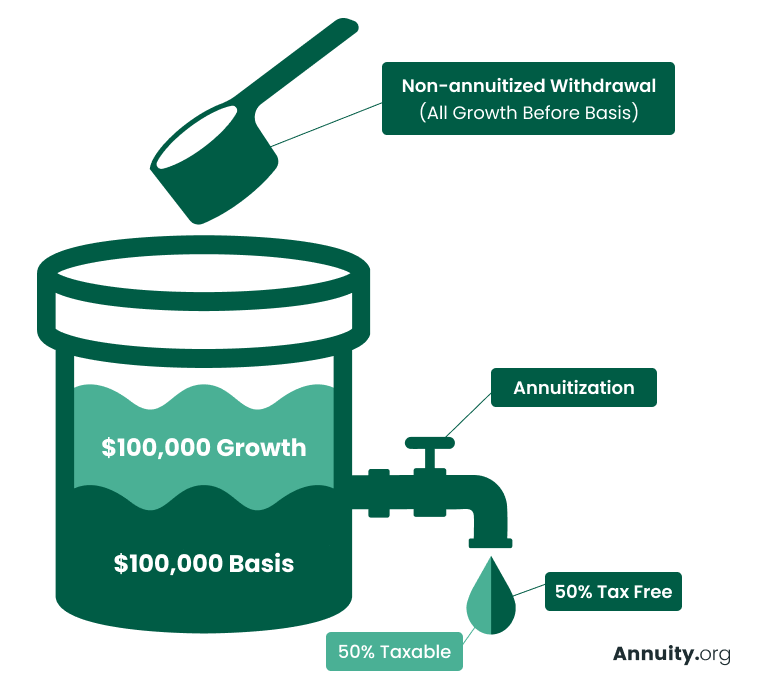

to be repealed in 2018, there is noabolition arranged for the New Jacket estate tax, Botwinick stated. There is no federal inheritance tax obligation. The state tax obligation gets on transfers to everyone apart from a specific course of people, he said. These include spouses, youngsters, grandchildren, parent and step-children." The New Jacket inheritance tax obligation applies to annuities equally as it relates to various other assets,"he stated."Though life insurance policy payable to a details recipient is exempt from New Jersey's estate tax, the exemption does not put on annuities. "Now, revenue taxes.Again, we're thinking this annuity is a non-qualified annuity." In short, the proceeds are strained as they are paid out. A part of the payment will be treated as a nontaxable return of investment, and the revenues will be taxed as normal income."Unlike inheriting various other possessions, Botwinick claimed, there is no stepped-up basis for inherited annuities. If estate taxes are paid as a result of the addition of the annuity in the taxed estate, the beneficiary might be entitled to a reduction for inherited revenue in regard of a decedent, he stated. Annuity settlements contain a return of principalthe cash the annuitant pays into the contractand passionmade inside the agreement. The rate of interest portion is taxed as average revenue, while the major amount is not exhausted. For annuities paying out over an extra extensive duration or life span, the principal part is smaller, leading to less tax obligations on the month-to-month settlements. For a wedded pair, the annuity contract might be structured as joint and survivor to make sure that, if one partner dies , the survivor will proceed to obtain guaranteed repayments and delight in the very same tax obligation deferment. If a recipient is named, such as the pair's youngsters, they come to be the recipient of an inherited annuity. Beneficiaries have numerous options to take into consideration when picking just how to receive cash from an inherited annuity.

{kind=link}

Table of Contents

Latest Posts

Exploring Annuities Fixed Vs Variable A Comprehensive Guide to Investment Choices Defining Fixed Index Annuity Vs Variable Annuity Advantages and Disadvantages of Different Retirement Plans Why Choosi

Breaking Down Your Investment Choices A Closer Look at Fixed Index Annuity Vs Variable Annuity Breaking Down the Basics of Investment Plans Features of Fixed Index Annuity Vs Variable Annuities Why Ta

Decoding How Investment Plans Work A Closer Look at Indexed Annuity Vs Fixed Annuity Breaking Down the Basics of Investment Plans Advantages and Disadvantages of Annuities Fixed Vs Variable Why Annuit

More

Latest Posts